Rebecca Jones, Co-Founder and CEO of objectsource, an Adobe Commerce (formerly Magento) agency, and Brian Gaynor, VP, Product and CEO EU of BlueSnap, a global payment provider, share insights on their recent collaboration. Together, they explore how objectsource’s new integration helps online merchants navigate the complexities of cross-border e-commerce by connecting Adobe Commerce to BlueSnap’s streamlined payment solutions.

Question: What are the biggest hurdles online merchants face when moving from local to international markets

Rebecca: When businesses expand internationally, they enter a more complex landscape, especially when it comes to payments. Adobe Commerce, including both the Magento Open Source and the licensed Adobe Commerce versions, offers robust features that support international growth. While the licensed version has strengths, such as enabling businesses to create country-specific sites and handle currency conversions, for some functionalities, there is little difference between the licensed and open-source versions. But that’s only part of the challenge. Payment processing becomes much trickier across borders. You often need separate payment providers for each country, and that can lead to a “Frankenstack” setup – a patchwork of providers, each with different logins, reconciliation steps and increased risks of errors. That’s why working with a global payment provider like BlueSnap can make all the difference. It keeps the payment flow centralised, reducing unnecessary complications.

Question: How does BlueSnap address the payment challenges that arise as businesses go global?

Brian: Managing payments across different regions without a unified system can lead to fragmented buyer experiences. Through our integration with Adobe Commerce and the module developed by objectsource, BlueSnap makes it possible for merchants to process payments seamlessly across multiple countries. Our solution keeps the checkout within the brand’s environment, improving customer trust and increasing transaction success rates. In addition, BlueSnap consolidates all transactions into a single system, which simplifies back-end processes, making things far easier for merchants who might otherwise struggle with regional payment differences.

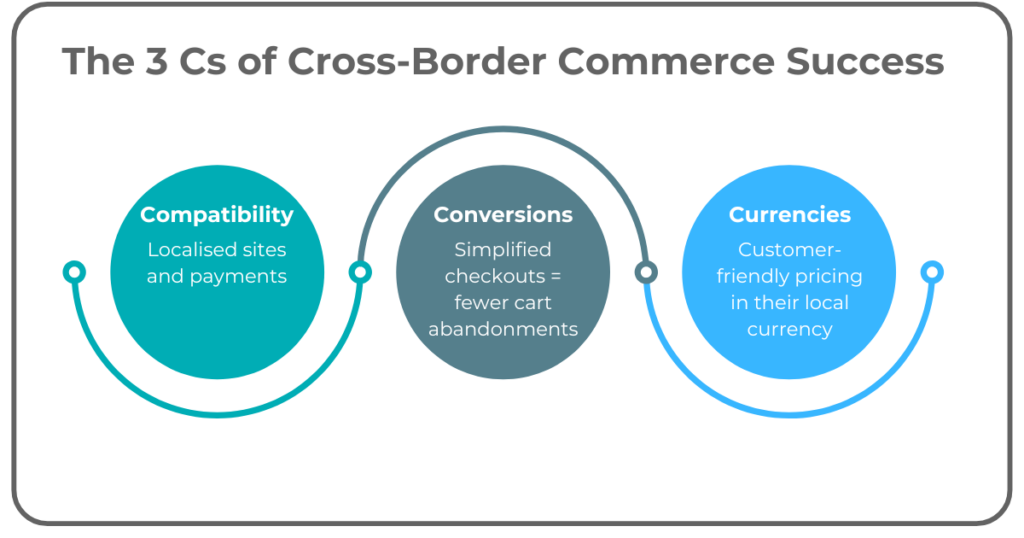

Question: How does this integration help merchants optimise across regions, specifically in terms of Compatibility, Conversions, and Currencies?

Rebecca: We often call these the “Three Cs.” First, Compatibility is crucial. Merchants need their website and checkout processes to feel localised, in terms of language, currency and adherence to regional regulations. Adobe Commerce’s customisation and multilingual options enable merchants to deliver this personalised experience. Our integration with BlueSnap extends this compatibility to payments, ensuring that the back end aligns with the front end for customers, no matter where they are.

Brian: Compatibility also involves supporting local payment preferences. Payment habits differ between regions – some European customers prefer direct bank transfers, while others might favour credit cards. BlueSnap automatically adapts to these regional preferences, boosting conversions by delivering a smoother checkout. Additionally, conversions are all about simplicity. An easy, seamless checkout means lower cart abandonment and higher conversion rates.

And the third “C,” currencies, is key for customer trust. Seeing prices in local currency reduces friction and reassures customers. BlueSnap supports a range of currencies, allowing merchants to receive payments in the currency they choose, which simplifies cross-border financial management.

Question: What impact does a fragmented, or “Frankenstack,” payment setup have on the customer experience?

Rebecca: Fragmented payment setups can disrupt the customer experience significantly. With a “Frankenstack” setup, customers are often redirected to external pages for payment processing, which breaks the flow of the checkout experience. This inconsistency can lead to customer hesitation, even cart abandonment. By integrating BlueSnap directly into Adobe Commerce, our module keeps customers within the merchant’s branded checkout flow. This not only keeps the experience consistent but also maintains customer trust, improving conversion rates.

Brian: Redirecting customers out of the site creates an unnecessary step in the checkout process, which can lead to doubt. Our integration with Adobe Commerce lets customers complete their purchases without ever leaving the site, reducing abandoned carts and instilling confidence. For merchants, this unified payment process also simplifies back-end management, so they can focus on growth rather than fixing disjointed systems.

Question: How do authorisation rates affect a merchant’s bottom line, especially for international transactions?

Rebecca: Authorisation rates have a direct impact on revenue. For example, if a business turns over £50 million annually and has an authorisation rate of 87.5%, this means that 12.5% of transactions are not going through which is an annual revenue loss of over £6 million. That’s a major hit, especially since authorisation rates often drop with cross-border transactions.

Brian: Right. When a transaction crosses borders, it goes through the cardholder’s bank, which assesses the risk before authorising it. International transactions sometimes appear as higher risk to banks, leading to declines. BlueSnap improves these authorisation rates by using local acquiring, which means routing transactions through local banks where possible. This not only reduces perceived risk, resulting in more approvals, but also allows merchants to reduce cross-border fees by up to 2% per transaction. Additionally, our failover system automatically retries declined transactions through a different bank, boosting the chances of success and further protecting revenue.

Rebecca: It’s about making every transaction count. When businesses optimise authorisation rates, they see a real impact on revenue and profitability.

Question: How does payment orchestration work, and how can it benefit merchants expanding globally?

Brian: Payment orchestration allows merchants to manage multiple providers and route transactions in ways that optimise success rates. Imagine a UK-based business expanding to France. They might initially experience lower conversion rates with French customers due to payment declines. With payment orchestration, they can route French customers’ transactions to local banks or payment providers. This approach – called intelligent routing – matches transactions to the customer’s local financial ecosystem, boosting authorisation rates.

In regions like the Netherlands, offering iDEAL, a local favourite payment method, can drastically increase conversions. BlueSnap’s orchestration handles these routing decisions for each region without requiring merchants to juggle multiple systems on their own.

Rebecca: This approach is very powerful. Payment orchestration is sophisticated, requiring specific technology and expertise, but BlueSnap has all of this in place. Merchants get the benefit of locally optimised payment routes without the complexity, which is invaluable when expanding internationally.

Question: What advice would you give Adobe Commerce store owners to help them optimise their payment strategies and improve customer experience?

Rebecca: Adobe Commerce offers a versatile, powerful platform for creating branded, tailored shopping experiences. With multicurrency and multilingual capabilities, store owners can build a site that appeals to global audiences. The integration with BlueSnap enhances this by supporting a smooth, unified checkout that fits the customer’s expectations, no matter where they’re located. Store owners can expand confidently, knowing that payments will be as seamless as the shopping experience they’ve created.

Brian: And from a financial perspective, BlueSnap makes life easier for finance teams. The only people who truly need to know that BlueSnap is in place are the finance team, who benefit from seamless reconciliations and a unified view of transactions across markets. This simplifies back-office work and frees up time for strategic initiatives, so they’re not spending time handling multiple reports and juggling spreadsheets.

Rebecca: Yes, it’s a solution that balances operational needs across the board. Store owners often focus on revenue and growth, but payment complexity can slow down finance teams. BlueSnap eliminates those obstacles, providing clarity in financial performance. The visibility and flexibility help Adobe Commerce merchants meet their objectives more efficiently.

Brian: At the end of the day, BlueSnap’s role is to “get the money in the door” efficiently and reliably. With optimised payment processing, high authorisation rates and simplified reconciliation, merchants have more control over their financial success and can focus on delivering a consistent and satisfying customer experience worldwide.

Rebecca: Thanks to Adobe Commerce (formerly Magento) and BlueSnap, our partnership is a win for merchants ready to expand their reach and grow their business globally.

Brian: Absolutely. With our combined solutions, merchants can simplify payments, grow their revenue and deliver a seamless experience for customers across borders. It’s a comprehensive approach to overcoming the challenges of international e-commerce.

To learn more about BlueSnap’s global payment orchestration platform, read Cross Border Payments with BlueSnap, integration by objectsource.

Find out more about the BlueSnap module on the Adobe Commerce Marketplace.

Contact us using the form below if you’d like more information or to discuss how objectsource can help you implement cross-border e-commerce for your business.